The Manhattan real estate market settled into its new normal during the first quarter, with slower activity transitioning to a seasonally active marketplace as the busy spring season started. This quarter’s headline is the 8.3% year-over-year decline in the median sales price, which was somewhat expected given the shift to lower volume throughout 2022. However, the median price per square foot proved more resilient despite the decline in activity, falling only 1% versus last year. Heading into Q2, expect closed sale prices to remain under pressure as comparisons to peak levels continue.

One of the most obvious details of the new market dynamics is the significant increase in days on the market reflecting the change in liquidity. It took sellers 111 days to sign a deal up in Q1, a 42% increase compared to last year and a 29% more than the previous quarter. That is just not a data point we are used to!

See the full report here: 1Q2023 Quarterly Report

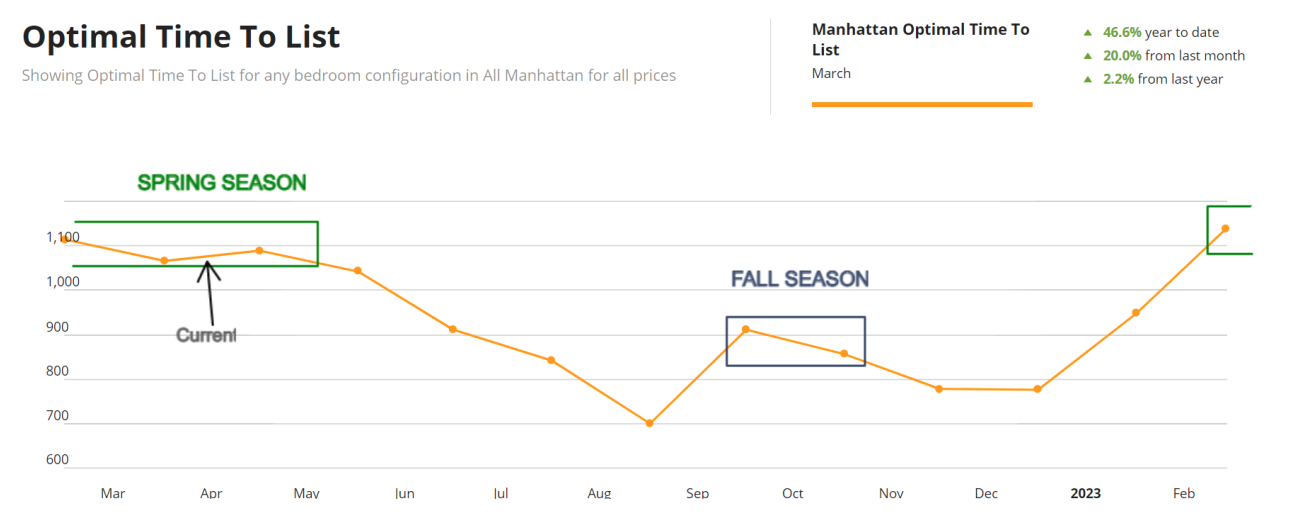

Peak Seasonality is Approaching

Manhattan is a seasonal market with two active seasons in the calendar year: spring & fall. The spring active season is longer duration & more active than the fall season. We are currently in the middle of the spring season and approaching our final six weeks of historically active deal volume. This suggests that as June rolls around, the level of liquidity/deals is likely to fall for the four consecutive summer months until the fall season begins in October. Here is the chart showing this dynamic:

www.urbandigs.com

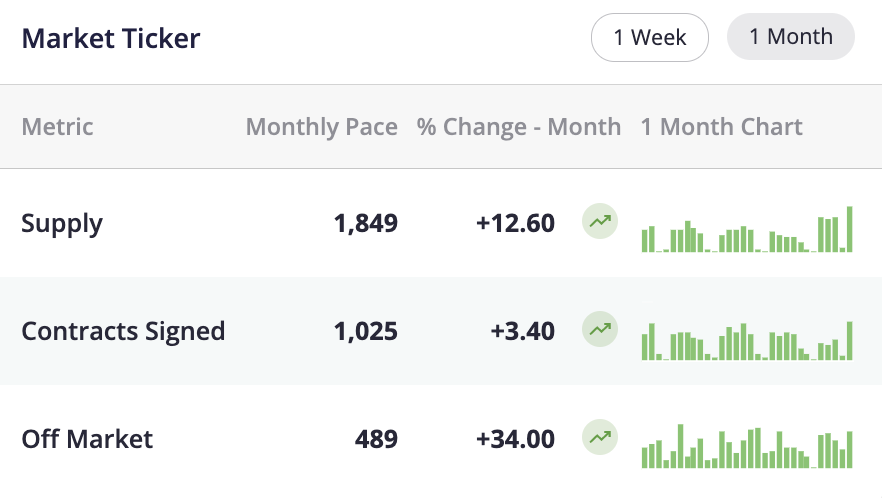

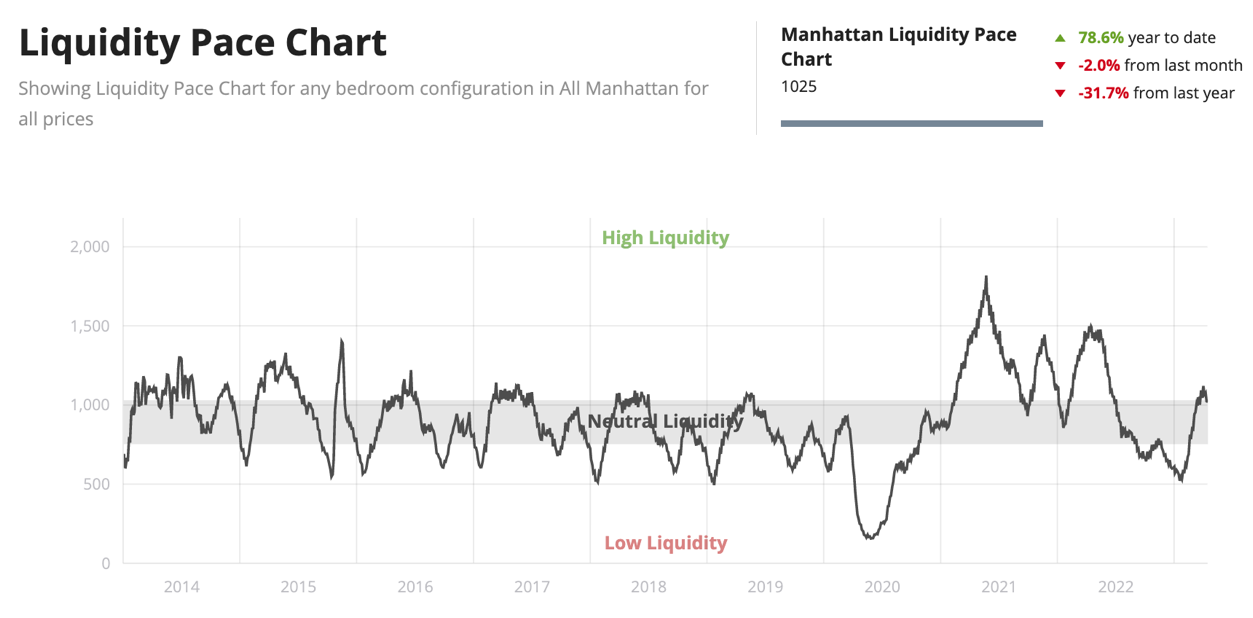

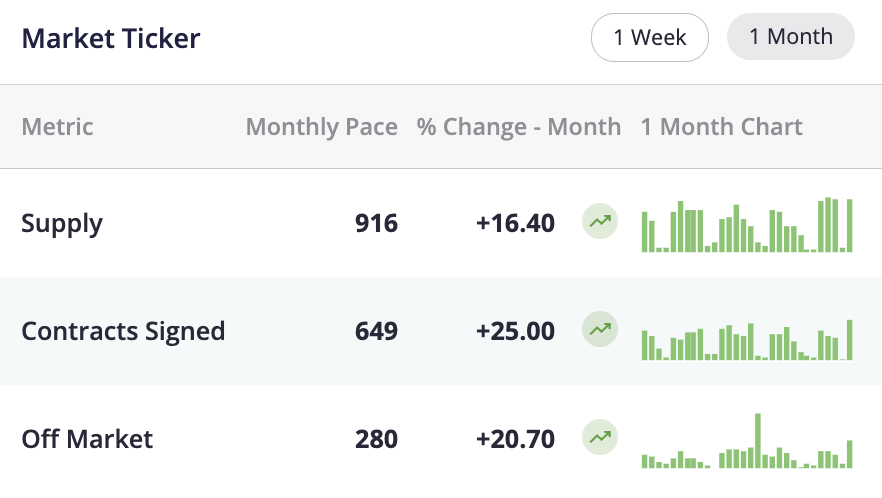

Manhattan vs Brooklyn Metrix:

The Manhattan market continues in solid net surplus territory – Supply (inventory) is larger than the combination of Contract Signed and Off Market. The wobble in the pace of liquidity suggests Manhattan may have seen its highs this season.

www.urbandigs.com

www.urbandigs.com

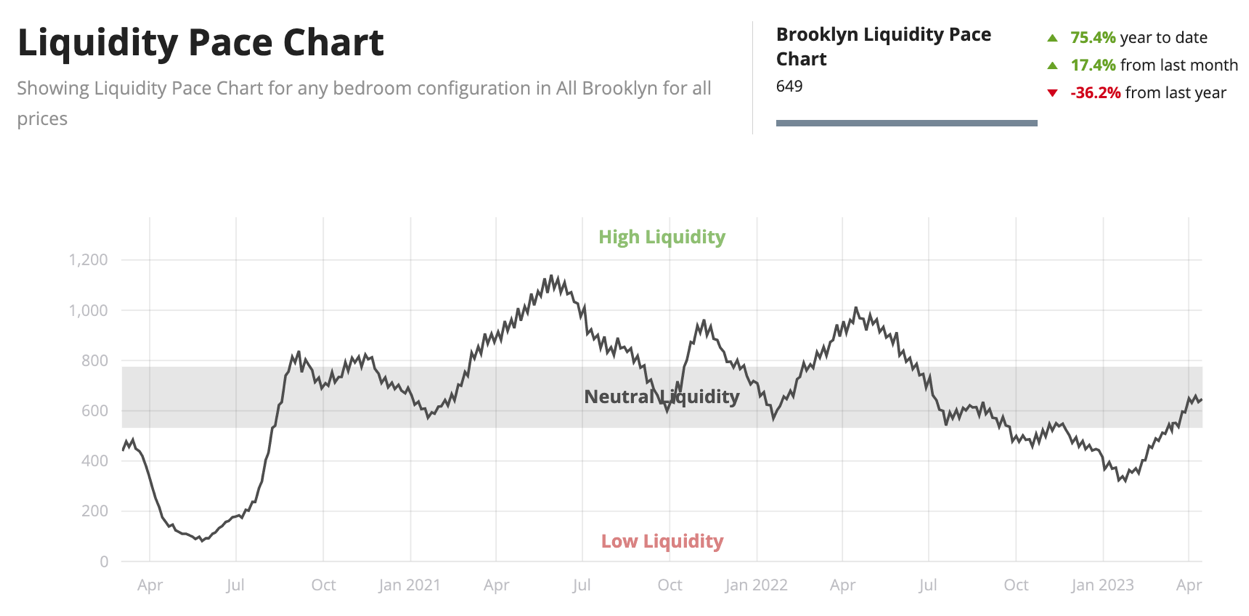

Brooklyn inventory ticks higher albeit slightly as supply remains lackluster. The liquidity pace in Brooklyn did not really surge and shows signs of topping out in the neutral range.

www.urbandigs.com

www.urbandigs.com

If you have questions, please call or email anytime.