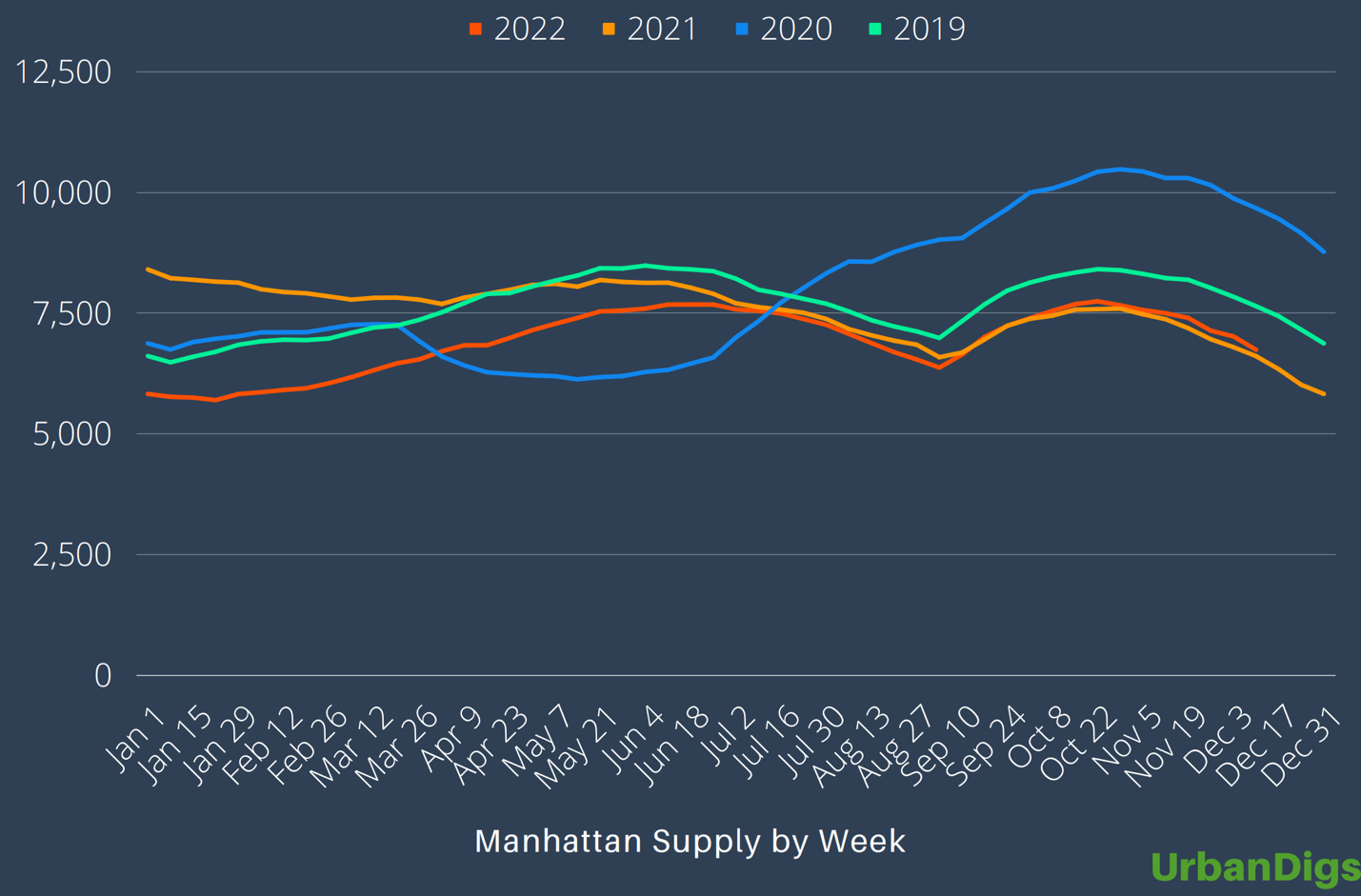

The story here is that low supply has been keeping the market in check. Supply has been moving in-line with 2021 numbers almost exactly since July. Because this has been following the seasonal curve, we treat this as uneventful. Having said that, we remain in a buyer’s market. Buyers currently have the leverage. For how long is the question?

Manhattan Supply by Week Chart:

www.urbandigs.com

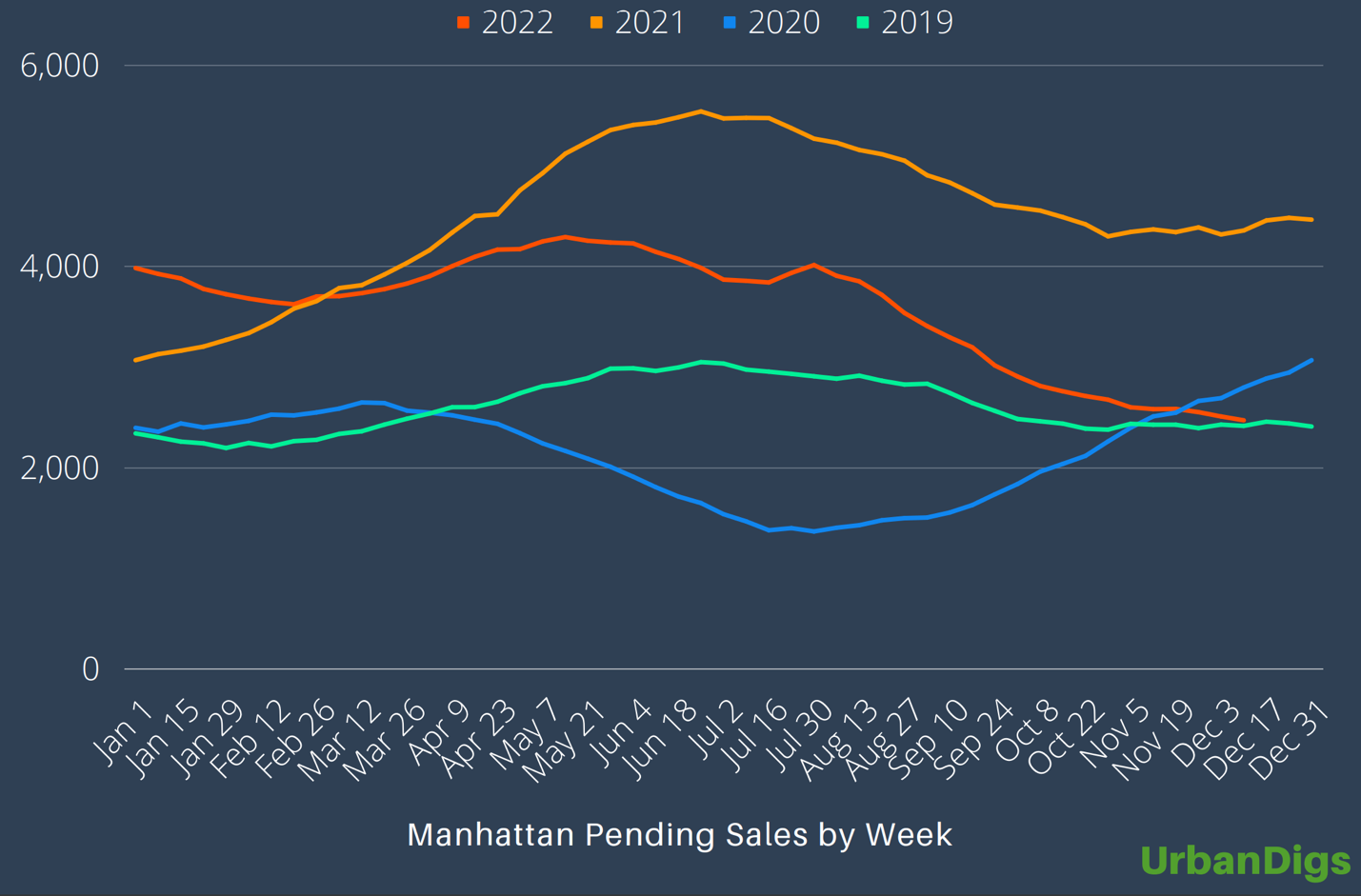

As transaction volume slows, there are certainly deals to be had for serious buyers. To be clear, there is no distressed selling happening in this market. If sellers are not getting their bid, they are more than likely coming off the market and waiting for the spring to re-list.

Do buyers still have the advantage in leverage right now? Yes. Despite that though, demand has continued to trend down and if it continues on its current path could end the year at its lowest point in 10 years.

Manhattan Pending Sales by Week Chart:

www.urbandigs.com

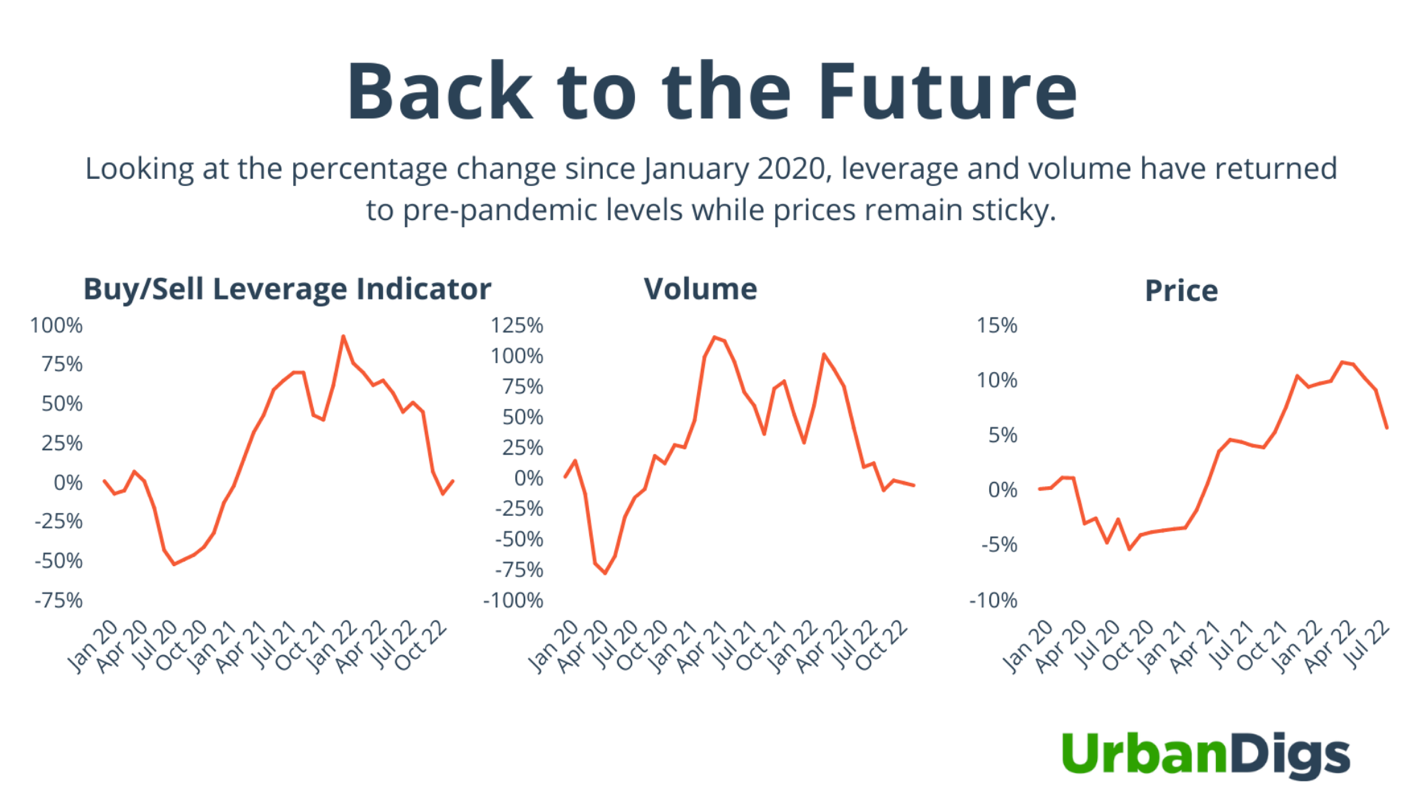

The charts below show a three-year look at leverage, volume, and price and paint an interesting picture of our recent markets:

- 2020 was Covid lockdown – we saw a drop in volume, price, and a swing from a seller’s market to buyer’s market

- 2021 saw off the chart deal volume due to pent up demand resulting in the return to a seller’s market. Volume climbs. Price increases. Bidding wars return

- 2022 – post 1st quarter – buyers regain leverage and volume decreases. Negotiating power for buyers remains 5-7% off ask. There is no panic selling.

www.urbandigs.com

It is looking like the summer of 2022 was the New York City market shift period with demand and prices softening. The fall through the end of 2022 will likely demonstrate the market stabilizing once the sales numbers come in. Pricing continues to be supported by low inventory.

The bottom line is 2023 will write its own story. We look forward to traveling this road with you and will continue to keep you informed as the data is released.

Wishing you and your family a wonderful holiday season!